Seeking a consolidation loan for bad credit in South Africa? High risk loans for blacklisted individuals often worsen debt through predatory rates. True relief comes from legal debt restructuring under the National Credit Act, which slashes your monthly installments, caps interest rates, and shields your assets without taking out new loans.

The search for a consolidation loan for bad credit in South Africa often stems from a place of deep financial desperation. For millions of South Africans, navigating the modern macroeconomic landscape is an uphill battle. With historical interest rate hikes, volatile inflation, and the steadily rising cost of basic living necessities, household budgets have been stretched far past their breaking points. Many individuals find themselves trapped in an exhausting cycle of juggling multiple high-interest short-term loans, store accounts, and credit card payments just to survive the month. In this high-stress environment, the marketing promise of “one easy monthly payment” feels like an absolute lifeline.

However, the structural reality of the lending environment in South Africa is significantly more complex and hazardous than glowing marketing slogans suggest. While the conceptual allure of rolling all your fractured debts into a single consolidated pool is highly appealing, the legal, mathematical, and financial mechanisms hidden behind these specialised bad credit loans can rapidly worsen the very problems they claim to resolve. For the average consumer already burdened with an adverse credit history, this supposed quick fix is frequently a financial mirage that completely vanishes upon a closer, more technical inspection of the underlying loan contract.

In the broader South African legal context, the National Credit Act 34 of 2005 (NCA) was explicitly enacted to safeguard consumers from predatory credit practices. This landmark piece of social legislation was specifically engineered to promote a highly fair, transparent, and non-discriminatory marketplace for access to consumer credit, while strictly prohibiting the destructive practice of reckless credit granting. Yet, despite these extensive, codified legal safeguards, the systemic market demand for high-risk loans for blacklisted consumers remains at an all-time high.

This overwhelming demand is routinely capitalised on by alternative fringe lenders, some of whom operate entirely on the outer periphery of regulatory compliance, or structure agreements that, while technically legal on paper, are entirely ruinous for the long-term financial health of the borrower. To successfully navigate this dangerous terrain, consumers must understand the fundamental, systemic distinction between entering into a brand-new credit agreement and utilising statutory debt relief.

A consolidation loan is, by its very legal definition, a completely new contract, a new debt instrument that you are actively taking on to liquidate old obligations. In stark contrast, legal debt restructuring is an established statutory remedy that systematically modifies your existing obligations. For a consumer who is already actively sinking into the quicksand of “bad credit,” the former is typically impossible to secure from reputable, low-interest banking institutions, whereas the latter is a constitutional and legislative right explicitly enshrined within the protective framework of the NCA.

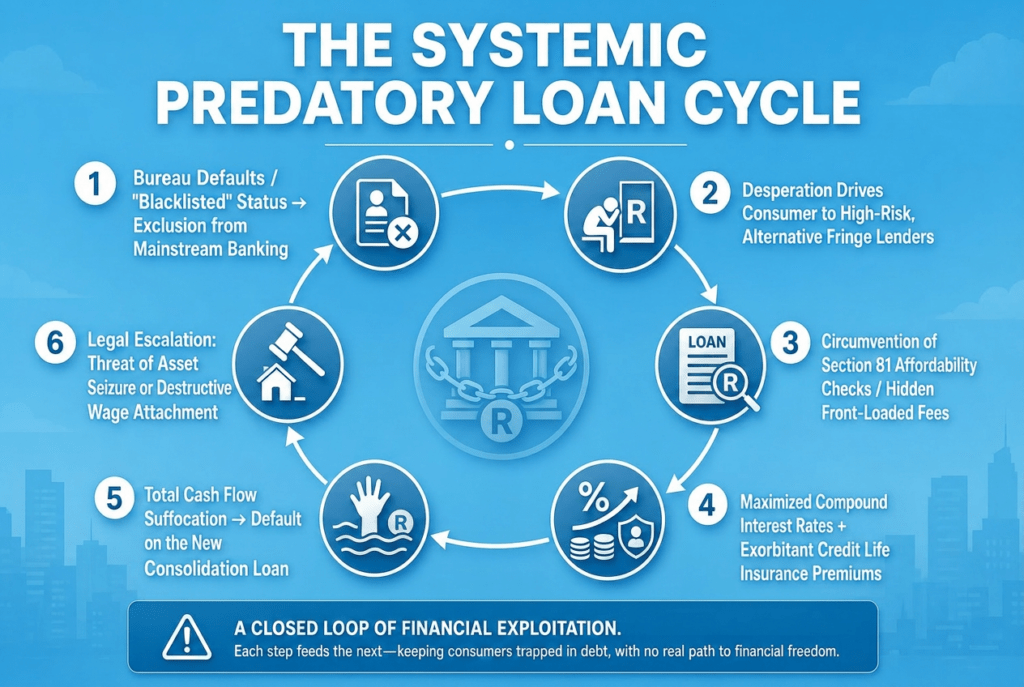

The trap of high-risk loans for blacklisted consumers

When financially vulnerable consumers turn to search engines to locate high risk loans for blacklisted individuals, they are immediately funneled into a targeted, highly predatory marketing ecosystem. In South Africa, the term “blacklisted” is a persistent colloquial myth that has absolutely no formal legal definition or standing under the NCA. What consumers refer to as being blacklisted is simply the presence of adverse credit indicators, default records, or low numerical credit scores held on the databases of major registered credit bureaus.

Fringe credit providers and informal, unregistered lenders colloquially known as “Mashonisas” deliberately exploit the panic associated with this “blacklisted” stigma. These predatory entities intentionally target their operations at consumers who have been rejected by traditional, risk-averse commercial banks. They systematically bypass or manipulate the rigid, mandatory affordability assessments strictly demanded by Section 81 of the National Credit Act. The structural trap of these high-risk financial products lies entirely within the true compound cost of the credit being offered.

Because the borrowing consumer is already deemed an extreme credit risk due to their historical bureau defaults, the alternative lender claims they must hedge their risk by implementing the absolute maximum legal interest thresholds permitted by the National Credit Regulator (NCR), alongside heavily front-loaded fees. In many illicit instances, lenders far exceed these legal caps. These operators use the consumer’s deep feelings of financial isolation as leverage to enforce terms that would be instantly rejected within a healthy, competitive financial ecosystem.

Beyond the baseline interest rates, these high-risk agreements are routinely packed with hidden structural costs. These include maximised initiation fees, ongoing monthly administrative service charges, and mandatory, exorbitantly priced credit life insurance premiums. The severe legal ramifications of failing to adhere to the strict consumer protection requirements of the NCA were brought to the forefront by the Constitutional Court of South Africa in the landmark matter of National Credit Regulator v Opperman.

In this pivotal case, the apex court dealt directly with the severe statutory consequences of an unlawful credit agreement entered by an unregistered lender. The Constitutional Court forcefully reinforced the core legislative principle that credit providers cannot simply circumvent or ignore the strict registration and affordability mandates of the NCA and expect the judicial system to protect their financial investments or validate their claims. The ruling made it explicitly clear that the court views consumer protection as a paramount public interest objective.

Historically, the predatory nature of high-risk alternative lending was further amplified by the widespread abuse of Emolument Attachment Orders (EAOs), commonly referred to by the public as “garnishee orders.” Unscrupulous lenders would routinely secure these orders through compliant, low-level clerk processes in distant jurisdictions, allowing them to deduct substantial loan installments directly from a worker’s monthly payroll before the employee even received their salary. This left thousands of families without sufficient resources to secure basic nutrition, transport, and shelter.

The legal landscape surrounding this practice was shifted by another monumental Constitutional Court victory in University of Stellenbosch Legal Aid Clinic v Minister of Justice and Correctional Services. The Constitutional Court ruled that the historic, unmonitored issuance of EAOs by court clerks was entirely unconstitutional. The court mandated that strict, individualised judicial oversight must occur before any EAO can be legally issued against a consumer’s wages.

The bench emphasised that a judicial officer must actively evaluate whether the deduction is truly just and equitable, ensuring that the consumer’s fundamental constitutional right to human dignity and physical livelihood is never compromised. Despite this massive victory for consumer rights, predatory high-risk lenders continually attempt to bypass these judicial speedbumps by coercing desperate borrowers into signing voluntary payroll deductions or complex, multi-layered debit order mandates, making the unregulated high-risk loan market an exceptionally dangerous minefield for uninformed consumers.

Why high-interest debt worsens cash flow

The primary, unassailable mathematical reason why a brand-new consolidation loan for bad credit in South Africa completely fails to restore a consumer’s financial stability is its immediate, negative impact on net monthly cash flow. High-risk consumer loans are structurally characterised by compressed, short-term repayment horizons coupled with maximised interest rates. When a distressed individual chooses to consolidate five or six separate, lower-interest obligations into a single, massive, high-interest “bad credit” consolidation loan, the overall total volume of interest paid over the life of the loan skyrockets.

This specific economic phenomenon is what financial experts classify as a terminal “debt spiral.” While the consumer experiences a brief, psychological sense of relief from making one monthly payment instead of dealing with five separate creditors, they are paying that single alternative lender significantly more money than the combined total of the previous five obligations.

According to official directives from the National Credit Regulator (NCR), formal reckless lending occurs legally when a credit provider fails to perform a comprehensive, objective affordability assessment, or when the evidence demonstrates that the consumer did not fully comprehend the risks, total costs, or long-term obligations of the underlying agreement. If a household is already actively struggling to meet basic, non-discretionary living expenses, adding a heavily front-loaded consolidation loan further depletes their remaining disposable income.

This severe cash flow suffocation forces the consumer to take out even more high-interest “payday” loans or micro-loans simply to service the monthly installment of the new consolidation loan. This creates a terminal financial feedback loop. The cash flow crisis is not just an abstract line item on a budget; it represents an irreversible “opportunity cost” for the household. Every single Rand swallowed up by excessive interest is a Rand completely stripped away from child education, healthcare, nutrition, or long-term retirement savings, effectively mortgaging the family’s future for a momentary, passing illusion of relief.

| Financial Indicator / Metric | High-Risk Consolidation Loan (New Credit) | Statutory Debt Restructuring (Debt Review) |

| Impact on Total Principal Debt | Increases significantly due to front-loaded fees. | Consolidates existing debt balances without adding new capital. |

| Applicable Interest Rates | Fixed at or above maximum NCR thresholds (up to 27%+). | Legally restructured down to significantly lower rates (often 0-5%). |

| Legal Asset Protection | None. Default leads to immediate summons and attachment. | Full statutory moratorium against litigation (Section 86). |

| Affordability Verification | Often bypassed or manipulated by alternative lenders. | Strict, objective court-ordered assessment of true living costs. |

| Effect on Monthly Cash Flow | Suppresses long-term cash flow via compounding interest. | Instantly frees up immediate cash flow via a single lower payment. |

A critical, yet widely misunderstood legal safeguard designed to protect consumer cash flow from this type of exploitation is the ancient common-law in duplum rule, which has been formally codified and strengthened within Section 103(5) of the NCA. This statutory rule explicitly dictates that all interest, initiation fees, service fees, and credit life insurance charges that accrue while a consumer is in default may never, in aggregate, exceed the remaining principal debt balance at the exact time of the default.

Predatory lenders routinely attempt to bypass this consumer shield by forcing struggling borrowers to “refinance,” “roll over,” or “consolidate” their defaulting accounts into brand-new agreements. This creates a brand-new principal loan balance, effectively resetting the in duplum interest clock. This deceptive practice is a direct violation of the core spirit and letter of the NCA. By gaining a clear understanding of these statutory mechanisms, consumers can easily identify when an advertisement for a consolidation loan for bad credit in South Africa is a predatory trap disguised as financial assistance. It is far more effective to learn how to pay off debt with low income through structured legal remedies rather than trying to borrow your way out of a deep financial crisis.

Safe alternatives to risky consolidation loans

Rather than pursuing high risk loans for blacklisted individuals, South African consumers should utilise the legal protections provided by the state. The single most effective, safe, and regulated alternative to a high-risk loan is the formal process of Debt Review, as meticulously outlined under Section 86 of the National Credit Act. Debt review is completely distinct from a consolidation loan because it is not a new loan. It is a highly formalised, court-supervised restructuring of your existing debt obligations.

It is a statutory remedy engineered specifically for consumers who find themselves in a genuine state of over-indebtedness. Unlike a risky consolidation loan, which depends entirely on a consumer’s ability to take on more expensive debt, debt review relies on your statutory right to pay only what you can afford after your non-discretionary household survival expenses have been fully covered.

In the landmark case of Sebola v Standard Bank, the Constitutional Court heavily emphasised the absolute necessity of credit providers strictly adhering to proper, formalised legal procedures before they can attempt to enforce debt obligations or repossess property. Debt review provides an immediate, powerful legal moratorium on all external enforcement actions. The exact moment a consumer formally applies to a registered debt counsellor, credit providers are legally barred from initiating new court summonses or executing asset attachments.

A qualified debt counsellor will perform an objective evaluation of your finances and use specialised software to negotiate directly with your creditors. This process can reduce interest rates frequently down to 0% for unsecured personal loans and credit cards while extending the overall repayment timelines. This newly structured, single payment plan is then officially submitted to the National Consumer Tribunal or a Magistrate’s Court to be locked in as a binding court order, ensuring the protection is permanent if the consumer adheres to the plan.

Another safe alternative available within the South African legislative framework is the “Debt Intervention” mechanism, which was introduced via the National Credit Amendment Act 7 of 2019. This statutory measure was specifically designed by lawmakers to assist low-income earners and vulnerable consumers who have no meaningful disposable income or assets to participate in traditional debt review. While the administrative rollout of debt intervention has been a gradual process, its inclusion in the law represents a clear acknowledgement by the government that high-risk consolidation loans are not a viable or sustainable solution for financially distressed individuals.

For severe, terminal instances of insolvency where a consumer’s total liabilities drastically exceed their entire asset base, sequestration under the Insolvency Act 24 of 1936 remains a final legal option. However, because sequestration involves the forced surrender of your entire estate to a court-appointed trustee and carries long-term legal restrictions, it is a drastic step. For most everyday consumers looking for a consolidation loan for bad credit in South Africa, formal debt review stands as the definitive gold standard of safe financial relief. It allows for the methodical, dignified repayment of debt without ever needing to take on a single cent of fresh borrowing.

The comprehensive South African consumer protection framework remains heavily underutilised simply because everyday consumers are unaware of their extensive statutory rights. One of the most potent legal tools available under the NCA is the concept of “reckless credit.” Under Section 80 of the Act, an agreement is legally deemed reckless if the credit provider completely failed to perform a valid affordability assessment, or if the evidence demonstrates that the consumer did not fully understand the true risks and costs, or if entering into that agreement directly caused the consumer to become entirely over-indebted.

If a Magistrate’s Court or the National Consumer Tribunal determines that a credit agreement was granted recklessly, they possess the full statutory power to suspend or set aside the consumer’s obligations under that specific agreement. This is a critical consideration for anyone holding high-risk loans, as a significant portion of alternative bad credit products fail to meet these strict underwriting guidelines.

Furthermore, the state implemented a major regulatory “credit amnesty” through the Removal of Adverse Consumer Credit Information and Information Concerning Paid-up Judgments Regulations. This initiative was designed to give consumers a fresh start by ordering credit bureaus to remove historical negative listings. However, as explicitly noted by the Minister of Trade and Industry during its implementation, removing a listing from a bureau profile does not cancel the underlying legal debt.

Consumers frequently confuse the removal of an adverse listing with the total cancellation of their debt, leading them to search for fresh high-risk loans for blacklisted individuals when they should be focusing entirely on settling their existing obligations through sustainable means. Your credit score is simply a reflection of your underlying financial behavior; no quick-fix loan can repair it. Only consistent, structured, and affordable repayment through a process like debt review can truly restore your financial standing.

Finally, the case of Ferris v First Rand Bank serves as a vital cautionary reminder for consumers navigating debt restructuring. The Constitutional Court ruled that if a consumer enters a court-ordered debt restructuring plan and subsequently breaches those terms, the credit provider is legally entitled to instantly enforce the original credit agreement without providing further statutory notice.

This underscores the fact that while legal alternatives to consolidation loans are incredibly powerful, they require long-term financial discipline from the consumer. The path to true financial freedom in South Africa is firmly paved with consumer protections, but it requires individuals to break free from a “new loan” mindset and embrace sustainable, structured repayment plans.

FAQs: Bad Credit Consolidation

High-risk consolidation loans carry maximum legal interest rates, front-loaded initiation fees, and expensive credit life insurance policies. Because they represent a brand-new credit agreement rather than a restructuring of existing debt, they fail to address the root systemic causes of household over-indebtedness. Borrowers frequently discover that the new consolidated monthly installment is still entirely unaffordable relative to their true living expenses. This forces them to secure additional high-interest short-term payday loans just to pay the installment on the consolidation loan, trapping them in a destructive debt spiral where they constantly borrow fresh capital simply to service compounding interest.

While select alternative providers offer legal high-risk products for consumers with poor credit scores, most advertisements promising “guaranteed approval for blacklisted individuals” or “loans without credit checks” originate from unregistered, predatory lenders known as Mashonisas. Legitimate credit providers in South Africa must be registered with the National Credit Regulator (NCR) and are strictly obligated by Section 81 of the National Credit Act to perform rigorous affordability tests before granting credit. Any lender attempting to bypass these mandatory credit bureau assessments is operating unlawfully and should be entirely avoided to prevent severe financial exploitation.

Debt restructuring, such as Debt Review under Section 86 of the National Credit Act, is a formalised legal process that renegotiates the repayment terms of your existing debts to make them affordable. It does not involve borrowing any new money or taking on new contracts. Instead, it reduces interest rates and extends repayment timelines under court protection. Consolidation loan, conversely, is a brand-new credit agreement where you borrow fresh capital at a high interest rate to pay off old lenders. For someone with an adverse credit history, this new loan will almost always feature significantly higher interest rates and fees than the original debts combined.